Just a few months back, we heard many stories of mass layoffs amid the financial crisis crippling the world. It was not just the startups, even industry giants like Microsoft, Google, and Amazon had to cut their numbers in response to the global economic crisis. It seems like uncertainty is becoming an increasing noise in today’s rapidly changing world. In such a scenario, how do you stay afloat, let alone meet your financial goals? The answer is having an emergency fund. Check out this blog to know all about having an emergency fund and how to build this financial armour to fight against the tough times that may lay ahead.

Read More: What is Life Stage Investing?

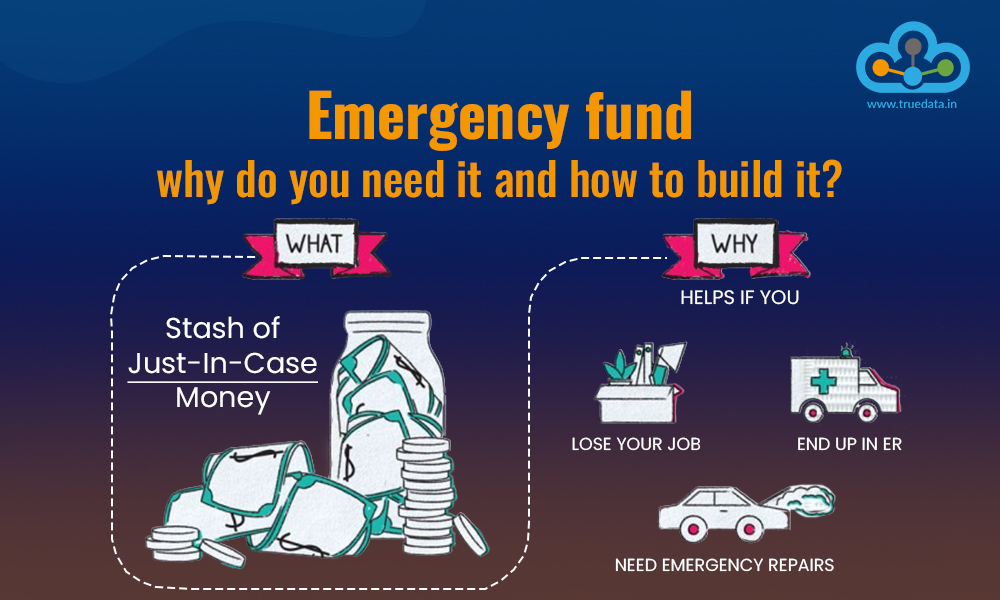

The concept of an emergency fund is not new but an age-old concept in financial planning. We have all seen our mothers stashing a portion of savings in flour or rice dabbas and suddenly producing it the time of an urgent need. Now we have come a long way from these modes of creating an emergency find but the essence is still the same. An emergency fund is a safety net of financial security in times of unfortunate situations like a job loss or the loss of the sole earning member of a family due to death or an accident. It helps the person and their family to stay afloat till the time of a new job opportunity or seeking other avenues of finances.

After learning the meaning of an emergency fund, the next obvious question is how much is enough? While there is no ideal answer to this question, most experts believe that having a fund that is equal to approximately 6 months to 12 months of monthly income should be considered ideal to tide the period of uncertainty without any difficulty. This fund needs to be set aside taking into account the mandatory and essential expenses of the family on a monthly basis as well as a small buffer for any sudden or immediate needs. Another important point to understand is that an emergency fund is not the same as a simple savings account. It is a strategically planned fund that should meet the essential parameters like the safety of the corpus at the same time give some nominal returns on the investment. Therefore it is essential to invest in assets or securities that meet these criteria after careful consideration.

The youth today is well aware of the need for proper financial planning. Creating an emergency fund is part of this financial planning and therefore needs a thorough understanding of necessary factors. Some of these factors to consider while creating an emergency fund are explained hereunder.

The first step of building an emergency fund is analysing the monthly expenses and the living costs of the person or the family. An important point to consider in this regard is the segregation of the monthly expenses into essential categories like needs, wants and desires. The 50/30/20 rule of budgeting can be used for this purpose which will allow the optimum allocation of resources towards the fund's utilisation. A detailed budget can provide insights into discretionary and non-discretionary spending, allowing individuals to identify areas where they can cut back if necessary.

The stability of one's job plays a pivotal role in determining the size of their emergency fund. Jobs characterised by volatility or seasonal in nature or industries prone to economic downturns necessitate a more substantial financial cushion. Assessing job stability is crucial for evaluating the risk of sudden income loss, guiding individuals, particularly those in the freelance or gig economy, to determine the adequacy of their emergency fund in withstanding potential employment fluctuations. This understanding is essential for ensuring financial resilience during lean periods with irregular income patterns.

Health-related emergencies can bring about substantial expenses, underscoring the importance of having a financial cushion that can effectively cover potential medical bills. A prudent approach involves a thorough understanding of one's health insurance coverage, coupled with the assurance that the emergency fund is capable of bridging any gaps in coverage or addressing unexpected health-related expenditures. This meticulous consideration in financial planning ensures a comprehensive and resilient strategy, guarding against the financial impact of unforeseen medical circumstances. By having an emergency fund that is well-equipped to handle healthcare costs, individuals can navigate health-related challenges with greater financial security and peace of mind.

Effective emergency fund planning involves a careful balance between financial goals and debt obligations. It's crucial to distinguish between the emergency fund and savings earmarked for specific objectives like education, homeownership, or entrepreneurial pursuits. By clearly delineating these financial goals, individuals can allocate resources strategically and avoid tapping into funds reserved for specific aspirations in times of crisis. Moreover, managing debt obligations is integral to the emergency fund strategy. Ensuring that the fund not only covers immediate living expenses but also includes the ability to meet essential debt payments during financial hardships is paramount. This comprehensive approach not only safeguards against unforeseen challenges but also fosters a more structured and resilient financial plan, enabling individuals to navigate both short-term emergencies and long-term financial objectives with prudence and foresight.

Inflation is part of our daily lives and cannot be ignored. Therefore an effective emergency fund should also account for inflation so it can be a realistic allocation of resources and meet its purpose in a true sense. The relentless rise in the cost of living over time underscores the need for periodic reviews and adjustments to the size of the emergency fund. Inflation erodes the purchasing power of money, and a stagnant emergency fund may become inadequate to cover escalating expenses during unforeseen circumstances. Furthermore, a keen understanding of prevailing economic conditions is crucial for anticipating potential challenges that may impact financial well-being. By staying attuned to economic trends, individuals can proactively adapt their emergency fund strategies to ensure that it remains a robust and resilient financial buffer capable of addressing the evolving financial landscape as well as effectively weathering economic uncertainties.

Finally, the investment approach is pivotal in meticulous emergency fund planning, emphasising the crucial need for liquidity in assets. If a significant portion of savings is tied up in less liquid investments, recognizing the time required to convert these assets into cash during emergencies is vital for maintaining financial flexibility. Striking a balance in the investment strategy is essential to ensure returns while maintaining quick access to liquid funds. A thoughtful analysis of investment portfolios guides the determination of an appropriate emergency fund size, considering financial goals, risk tolerance, and the necessity for readily available funds during unforeseen circumstances.

After understanding the basic details of emergency funds, let us now focus on a few popular investment options to create this fund. Some examples of such investment options for this purpose are mentioned below.

One of the most straightforward and readily accessible options for parking emergency funds in India is a savings account. Banks across the country offer savings accounts with minimal to no risk, providing easy liquidity. While the interest rates on savings accounts may be lower compared to other investment options, they ensure quick access to funds during emergencies. This option is ideal for individuals who prioritise liquidity and safety over higher returns.

Fixed deposits are a popular choice for conservative investors seeking a balance between returns and safety. Banks and post offices in India offer fixed deposits with predetermined interest rates and tenures. The principal amount is safeguarded, and the interest earned provides a modest return. FDs are considered low-risk investment options with flexible tenures, making them suitable for emergency funds with a slightly longer investment horizon compared to savings accounts.

Liquid mutual funds offer a middle ground between traditional savings accounts and more complex investment options. These funds invest in short-term, highly liquid money market instruments. They provide better returns than savings accounts while maintaining relatively low risk. Liquid mutual funds in India allow for quick redemptions, making them suitable for emergency funds requiring a higher potential return without sacrificing accessibility.

Ultra short-term debt funds invest in debt securities with short maturities, offering a balance between safety and returns. These funds are known for providing slightly higher returns than traditional savings accounts and fixed deposits. They are relatively less volatile than equity funds, making them a suitable option for emergency funds. Investors should, however, be mindful of interest rate risks associated with these funds.

Gold Exchange-Traded Funds (ETFs) provide exposure to the gold market without the physical ownership of the metal. Investing in gold ETFs can serve as a hedge against inflation and economic uncertainties. While the liquidity of gold ETFs depends on market conditions, they offer a diversified option for emergency funds in India.

Building an emergency fund demands a holistic understanding of one's financial landscape. It is an essential part of an optimum financial plan that not only allows robust financial security in any unfortunate event but also inculcates a life-long habit of managing finances prudently.

This article is a brief attempt to provide the basics of an emergency fund and how to build it effectively. Let us know if you have any queries regarding the same or need any further information on this topic.

Till then Happy Reading!

Marisha Bhatt is a financial content writer @TrueData.

She writes with the sole aim of simplifying complex financial concepts and jargon while attempting to clarify technical and fundamental analysis concepts of the stock markets. The ultimate goal is to spread vital knowledge and benefit the maximum audience. Her Chartered Accountant background acts as the knowledge base to help clarify crucial concepts and create a sound investment portfolio.

The stock market in India has fascinated general Indian masses for long, perhap...

Most Often, gold and stocks are the investment showgrounds that attracts Indian ...

For analyzing the stock markets, Fundamental Analysis and Technical Analysis are...

A phenomenon of Open v/s high low When you are into the work of stock trading, ...